FIRE Calculator India — Financial Independence & Early Retirement Planning

Calculate your FIRE number, years to retirement, and personalised FIRE Health Score in real time. India-specific SWR, all 8 FIRE types — Lean, Coast, Barista, Fat FIRE and more. No login. All calculations on your device.

India's Most Comprehensive FIRE Calculator

8 FIRE types · 5,000 Monte Carlo simulations · India-specific 3.5% SWR · FIRE Health Score · 58 tested formulas

New to FIRE? Learn the basics▼

FIRE (Financial Independence, Retire Early) means building enough invested wealth that your portfolio returns cover your living expenses — so work becomes optional.

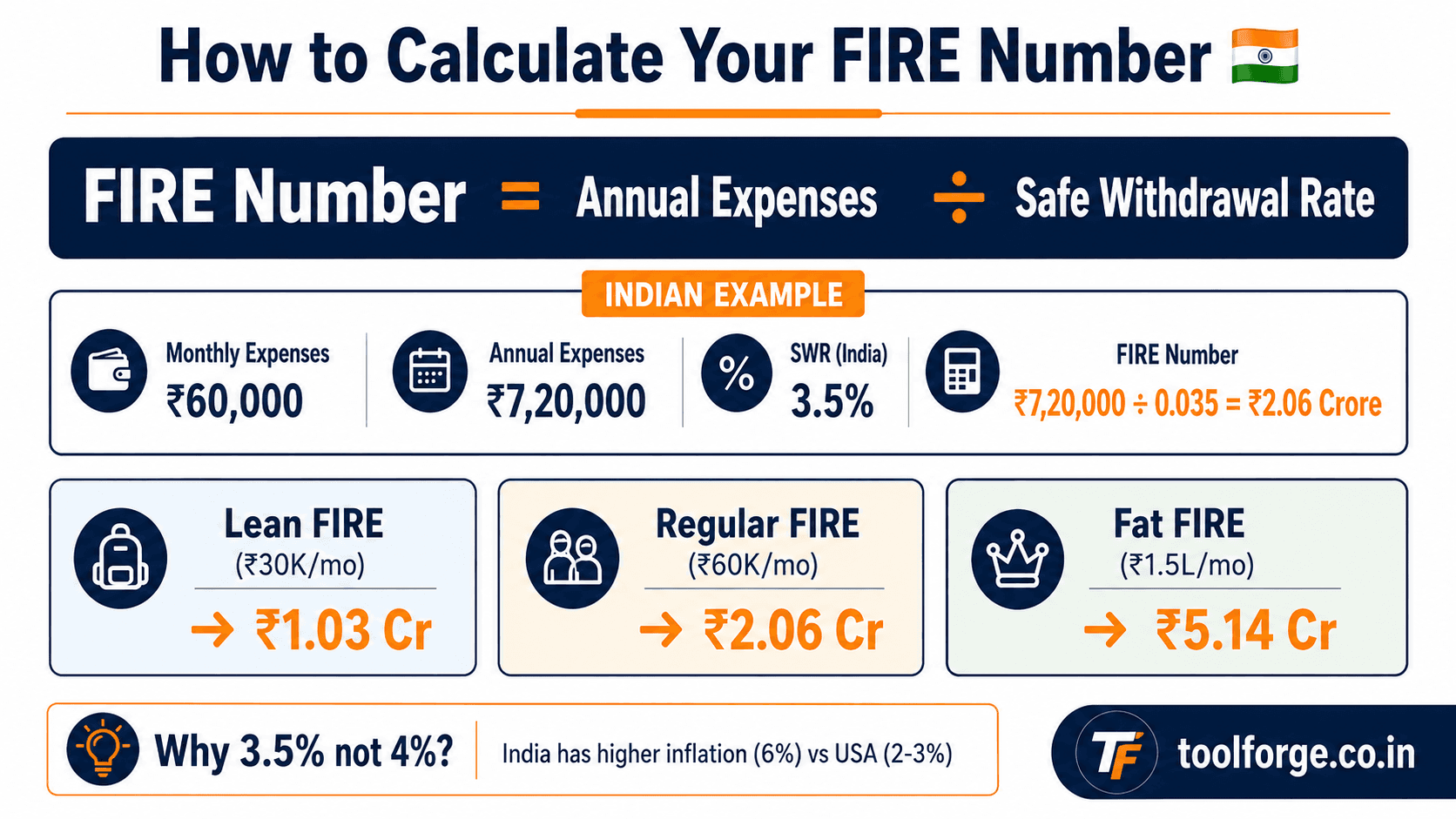

Your FIRE number = annual expenses ÷ Safe Withdrawal Rate (SWR). At 3.5% SWR, spending ₹60,000/month needs a corpus of about ₹2.06 crore.

The fastest path: maximise your savings rate and invest consistently in equity mutual funds via SIP. Use the SIP Calculator to project how your monthly SIP compounds over time.

Input mode

6 essential inputs only. Switch to Advanced for inflation, asset breakdown, SWR, and protection settings.

Quick-fill a scenario

🇮🇳 Free to use · No signup · All calculations run in your browser

About You

Income & Investments

Total monthly amount you invest (SIP in equity MFs, NPS, PPF, etc.) — compounded at your 12% pre-retirement return.

Savings rate: 30.0% 👍 Good

Current Wealth

Add up MF + stocks + EPF + PPF + FD + gold + any other investments

Effective real returns (after inflation)

Pre-retirement

6.0% real

12% − 6% inflation

Post-retirement

1.0% real

7% − 6% inflation

All corpus values shown in today's purchasing power.

Regular FIRE in

21.8 yrs

Age 52

Target Corpus

₹1,71,42,857.14

at 3.5% SWR · today's money

Progress to FIRE

2.9%

Monthly Expenses

₹50,000.00

₹6,00,000.00/yr

You are 2 years behind your target

At current pace: FIRE at age 52 · Target: age 50

Practical ways to reach FIRE by age 50:

💡 Increase monthly SIP by ₹5,000.00 — target a salary increment or bonus to fund this.

🧑💻 Start a side income of ₹4,000.00/month (freelance, consulting, tutoring) and invest it entirely.

📈 Target a 17% salary hike — an increment of this size would close your FIRE gap.

All 8 FIRE Paths

Lean FIRE

Age 49

₹1,37,14,285.71

Minimal lifestyle, retire faster

Regular FIRE

Age 52

₹1,71,42,857.14

Current lifestyle in retirement

Fat FIRE

Age 58

₹2,57,14,285.71

Upgraded lifestyle in retirement

Coast FIRE

⚠️ Not yet on track

₹1,71,42,857.14

Need ₹1,71,42,857.14 to coast

Barista FIRE

Age 48

₹1,20,00,000.00

Part-time covers 30% of expenses

Slow FIRE

Age 55

₹2,05,71,428.57

Gradual transition with lifestyle buffer

Geo-Arb FIRE

Age 46

₹1,02,85,714.29

Relocate to a lower-cost Indian city

Expat FIRE

Age 42

₹68,57,142.86

Retire in SE Asia or similar

Corpus Projection — 5,000 Scenarios

Shaded band = 50% of simulations. Dashed lines = 10th and 90th percentile.

FIRE Health Score

Fair

Across 7 financial dimensions

Health Score Breakdown

Your Top 3 Improvements

Corpus Progress (1/20 pts)

Add lump sums (bonuses, windfalls) to your corpus. Staying consistent with SIP through market dips compounds massively over time.

Income Streams (3/10 pts)

Add a side or passive income stream. Even ₹5,000–10,000/month from freelancing, rentals, or dividends materially reduces corpus depletion risk.

Insurance (5/10 pts)

Get term insurance (10–15× annual income) + family health floater (₹10–20L). One uninsured event can wipe out years of savings.

Smart Insights

Calculator v3.1 · Methodology updated Jun 2026 · All calculations run locally in your browser.

Results are for illustrative purposes only. Not SEBI-registered investment advice. Consult a SEBI-registered financial advisor before making investment decisions. Returns shown are not guaranteed.

Corpus at Key Ages

| Age | Projected Corpus | Progress to FIRE |

|---|---|---|

| Age 30 | ₹5,00,000.00 | 3% |

| Age 35 | ₹26,98,466.00 | 16% |

| Age 40 | ₹56,40,510.00 | 33% |

| Age 45 | ₹95,77,628.00 | 56% |

| Age 50 | ₹1,48,46,381.00 | 87% |

| Age 52 🎯 | ₹1,74,22,993.00 | 100% |

| Age 55 🎯 | ₹2,18,97,160.00 | 100% |

What-If Scenario Playground

Tweak any variable across 3 scenarios and compare outcomes in real time. Click a name to rename it.

Monthly Savings

Monthly Expenses

Expected Return

FIRE In

21.8 yrs

Age 52

Target

₹1,71,42,857.14

Real Return

6.0%

Lean FIRE Age

49

Progress

3%

Monthly Savings

Monthly Expenses

Expected Return

FIRE In

17.4 yrs

Age 48

Target

₹1,71,42,857.14

Real Return

6.0%

Lean FIRE Age

45

Progress

3%

Monthly Savings

Monthly Expenses

Expected Return

FIRE In

19 yrs

Age 49

Target

₹1,37,14,285.71

Real Return

6.0%

Lean FIRE Age

47

Progress

4%

💡 Scenarios are independent — changes here do not affect your main calculator above.

Family Planning

Add family goals to see their impact on your FIRE timeline

House Purchase Planning

Model the impact of a future home purchase on your FIRE timeline

Was this tool helpful?

How to Use This FIRE Calculator

- 1Enter your current age and the age at which you want to achieve financial independence.

- 2Add your annual income and monthly savings — the savings rate is calculated automatically and shown in real time.

- 3Enter your total current corpus — add up all investments: EPF, PPF, mutual funds, stocks, FDs, gold, and any other savings.

- 4Set your equity allocation percentage and expected annual return rate. Use 10–12% for a diversified equity portfolio.

- 5Fill in the Protection Checklist — emergency fund, insurance, and debt. These determine your FIRE Health Score.

- 6View your FIRE Health Score, years to FIRE, corpus target, and compare all 8 FIRE paths in the cards below.

What is FIRE? — Financial Independence, Retire Early

FIRE is a financial movement built around a simple but powerful idea: accumulate enough wealth that your investment returns cover your living expenses indefinitely — freeing you from the need to work for money. You are financially independent (the FI part) and can choose to retire early (the RE part), work part-time, pursue passion projects, or anything else.

The FIRE India movement 🇮🇳 has been growing rapidly among salaried professionals, freelancers, and entrepreneurs who recognise that India's equity markets, low cost of living relative to income, and a young working-age population create uniquely powerful conditions for early retirement. Communities like r/FIREIndia and r/IndiaInvestments are filled with Indians in their 30s who have already achieved financial independence — many on ₹15–25 LPA salaries.

FIRE does not mean living miserably or hoarding every rupee. It means building a large enough corpus — your “FIRE number” — that your money works for you instead of the other way around. The mathematical foundation is the Safe Withdrawal Rate (SWR): if your corpus is 28–33× your annual expenses, you can withdraw 3–3.5% per year and your corpus should last 30–50 years or longer.

The FI Part

Financial Independence = your investment returns cover your living costs. You no longer depend on a salary. This is the measurable goal.

The RE Part

Retire Early = you choose when, how much, and whether to work. Many FIRE achievers still work — on their own terms.

FIRE Number Formula & Calculation Method

The FIRE number is calculated using the perpetuity formula derived from the Safe Withdrawal Rate:

FIRE Corpus = Annual Expenses ÷ SWR

Annual Expenses = your monthly expenses in retirement × 12

SWR = Safe Withdrawal Rate = 3.5% (India-specific, vs 4% US rule)

Example: ₹60,000/month × 12 ÷ 0.035 = ₹2.06 crore

Years to FIRE is calculated by solving the Future Value (FV) formula for n:

FV(n) = C × (1+r)ⁿ + S × [(1+r)ⁿ − 1] / r

C = current corpus | S = annual savings | r = annual return rate

We find the smallest n where FV(n) ≥ FIRE Corpus.

Compounding frequency: Annual compounding is used for all projections. Monthly SIP contributions are treated as a single annual lump sum for calculation simplicity. For a 20-year horizon this produces results approximately 6–8 months later than monthly-compounding calculators (such as ET Money or Groww) using the same inputs.

Why 3.5% SWR for India?

India's average CPI inflation (5–7%) is higher than the US (2–3%). The original 4% rule was derived from US data. A 3.5% SWR provides an extra buffer against India's higher inflation and rupee depreciation risk.

FIRE Health Score

A proprietary 0–100 composite score across 7 dimensions: savings rate, corpus progress, asset allocation, emergency fund, insurance, debt position, and income streams.

Coast FIRE Formula

Coast Corpus = FIRE Target ÷ (1 + r)^years_to_retirement. Once your corpus reaches this level, compounding alone does the rest — no new savings needed.

Related tools that feed into your FIRE plan

Use the SIP Calculator to model the compounding effect of your monthly investments at different CAGR rates — the same math that powers the FIRE corpus projection above.

If you are deciding between an EMI (home loan or car) and continuing to invest, the EMI Calculator shows the full amortisation schedule so you can see exactly what each rupee of EMI costs your FIRE timeline.

Your savings rate — the most powerful FIRE lever — depends on your post-tax take-home. Use the Income Tax Estimator to compare Old vs New regime and find which gives you more monthly surplus to invest.

All 8 FIRE Types Explained

Lean FIRE

80% of current expensesLive below current means — no eating out, no subscriptions, low-cost accommodation. Best for those who value freedom above comfort. Achieved fastest but leaves no room for lifestyle inflation.

Regular FIRE

100% of current expensesRetire on your current lifestyle. The standard FIRE target — what most people mean when they say "FIRE number."

Fat FIRE

150% of current expensesRetire with a significantly upgraded lifestyle — premium travel, dining, domestic help. Requires a much larger corpus but gives maximum security and freedom.

Coast FIRE

VariesYour corpus is large enough that it will compound to your full FIRE target by retirement age — no new investments needed. You can work any low-stress job that covers current expenses.

Barista FIRE

70% covered by corpusSemi-retired — a part-time job or side income covers 30% of expenses, corpus covers the rest. Retire 5–10 years earlier than full FIRE by supplementing with light work.

Slow FIRE

120% of current expensesA gradual transition — you do not quit suddenly but wind down over time while building a larger corpus that allows lifestyle upgrades in later retirement years.

Geo-Arb FIRE

60% of current expensesRelocate to a Tier-2/3 Indian city (Coimbatore, Jaipur, Mysuru) where the same quality of life costs 40% less. Dramatically reduces required corpus.

Expat FIRE

40% of current expensesRetire abroad in low-cost countries — Bali, Chiang Mai, Da Nang — where ₹1–1.5 lakh/month provides a 5-star lifestyle. Requires careful tax planning for NRI status.

Worked Example — ₹15 LPA Salary, Retiring at Age 50

Scenario: Ravi, 30 years old, software engineer in Pune

Inputs

| Annual Income | ₹15,00,000 |

| Monthly Expenses | ₹50,000 |

| Monthly Savings | ₹45,000 |

| Current Corpus | ₹8,00,000 |

| Expected Return | 12% p.a. |

| Equity Allocation | 70% |

| Target FIRE Age | 50 |

Results

| Savings Rate | 36% |

| FIRE Corpus Needed | ₹1,71,43,000 |

| Annual Expenses in FIRE | ₹6,00,000 |

| SWR Used | 3.5% |

| Years to FIRE | ~14 years |

| FIRE Age | ~44 (ahead of target!) |

| Lean FIRE Age | ~41 |

At ₹45,000/month savings invested at 12% p.a., starting from ₹8 lakh corpus, Ravi reaches his ₹1.71 Cr FIRE target in approximately 14 years — at age 44, six years ahead of his target. Increasing savings by ₹10,000/month would bring this to age 42.

Common FIRE Planning Mistakes

Using the US 4% rule directly

India has higher inflation, rupee risk, and shorter market history than the US. The Trinity Study was built for US markets. Using 4% SWR for India overstates how much you can safely withdraw — 3–3.5% is more appropriate, meaning you need a larger corpus than the 4% rule suggests.

Not accounting for healthcare costs in retirement

Healthcare inflation in India runs at 10–12% per year — far above general CPI. Your expenses at age 60–70 will include significantly more medical spending than at age 35. Build a dedicated healthcare buffer of ₹20–30 lakh beyond your regular FIRE corpus, and maintain health insurance even after FIRE.

Forgetting that FIRE does not mean zero income

Many FIRE achievers pursue Barista FIRE or Slow FIRE — working part-time on passion projects, freelancing, or consulting. This dramatically reduces corpus requirements and also keeps the mind engaged. Treating FIRE as "never earn again" both overstates the corpus needed and makes the transition harder psychologically.

Ignoring sequence of returns risk

A market crash in the first 2–3 years of retirement can permanently impair your corpus even if long-term returns are fine. This is sequence-of-returns risk. Mitigate it by keeping 2–3 years of expenses in liquid/debt instruments at all times during retirement, so you never have to sell equity at a loss to cover expenses.

FIRE India Movement — Knowledge Base 🇮🇳

Explore our complete library of India-specific FIRE guides — each one covers the numbers, strategy, and real-world considerations for that FIRE type.

FIRE Number India

How much corpus you actually need to retire in India — with Indian inflation and SWR.

Safe Withdrawal Rate India

Why India uses 3–3.5% SWR instead of the US 4% rule — and what it means for your corpus.

4% Rule India

The Trinity Study rule adapted for Indian markets, inflation, and tax structure.

Lean FIRE India

Retire early on a minimal budget — what ₹20,000–40,000/month FIRE looks like in India.

Coast FIRE India

The point where your corpus grows to your FIRE target on its own — no more saving needed.

Fat FIRE India

Retire with a luxury lifestyle — ₹1.5–3L/month expenses and the corpus it requires.

Barista FIRE India

Semi-retire with part-time work covering some expenses — a smaller corpus, more flexibility.

FIRE Health Score

Score your FIRE readiness across 7 dimensions — and get a personalised action plan.

Frequently Asked Questions — FIRE Calculator India

Q: What is the FIRE number and how is it calculated?

Your FIRE number is the total investment corpus you need to retire and live off investment returns indefinitely. It is calculated by dividing your expected annual expenses in retirement by the Safe Withdrawal Rate (SWR). For example, if you need ₹6 lakh per year and use a 3.5% SWR, your FIRE number = ₹6,00,000 ÷ 0.035 = ₹1.71 crore. The logic: if your corpus is large enough, you can withdraw a small percentage each year and the remaining corpus continues to grow through returns — effectively lasting forever.

Q: Why does this calculator use 3.5% SWR instead of the US 4% rule?

The popular 4% rule comes from US research (the Trinity Study) based on US market and inflation data. India has historically higher inflation (5–7% CPI vs 2–3% in the US), rupee depreciation risk, less deep bond markets, and shorter track records for index funds. Indian FIRE researchers and financial planners generally recommend 3–4% SWR for India. This calculator uses 3.5% as a balanced, conservative default. You can adjust your monthly expenses to stress-test different effective withdrawal rates.

Q: What is the difference between Lean FIRE, Regular FIRE, and Fat FIRE?

These three FIRE types reflect different retirement lifestyles: Lean FIRE (80% of current expenses) means living minimally — cutting luxuries, cooking at home, avoiding discretionary travel. Regular FIRE maintains your exact current lifestyle with the same spending. Fat FIRE (150% of current expenses) means an upgraded retirement — business class travel, luxury experiences, help at home. Lean FIRE is reached fastest but sacrifices comfort; Fat FIRE takes longest but provides the most cushion.

Q: What is Coast FIRE and how do I know if I have achieved it?

Coast FIRE is the point where your current corpus, left to compound at your expected return rate, will grow to your full FIRE target by your planned retirement age — without any additional savings. Example: if you want ₹3 crore at age 55 and expect 12% returns, your Coast FIRE corpus at age 35 (20 years away) = ₹3 Cr ÷ (1.12)²⁰ ≈ ₹31 lakh. If you already have ₹31 lakh, you have achieved Coast FIRE — you could theoretically stop saving today and still retire on time. This calculator shows your Coast FIRE status automatically.

Q: What is Barista FIRE and how does it work?

Barista FIRE is a semi-retirement strategy where you quit your high-stress career but take a low-pressure part-time job that covers about 30% of your expenses. This means you only need corpus to cover the remaining 70%. For example, if your expenses are ₹60,000/month and your barista-style work earns ₹18,000/month, you only need corpus to generate ₹42,000/month. This significantly reduces the corpus needed and can allow you to "retire" 5–10 years earlier than full FIRE. It also provides social engagement, health insurance (if employer-provided), and prevents the psychological shock of full retirement.

Q: What is the FIRE Health Score and how is it calculated?

The FIRE Health Score is a proprietary 0–100 composite score calculated across 7 financial dimensions: Savings Rate (25 pts — targeting 40%+), Corpus Progress (20 pts — % of FIRE target reached), Asset Allocation (15 pts — equity % appropriate for your age), Emergency Fund (10 pts — 6 months expenses target), Insurance Coverage (10 pts — term + health), Debt Position (10 pts — penalises high-interest debt), and Income Diversification (10 pts — multiple income streams). Scores 80+ = Excellent, 65–79 = Good, 50–64 = Fair, 35–49 = Needs Work, below 35 = At Risk.

Q: Can I achieve FIRE on a ₹20 LPA salary in India?

Yes, absolutely. At ₹20 LPA, if you save aggressively — say ₹80,000/month (48% savings rate) — and invest at 12% CAGR, starting from zero corpus at age 28: your FIRE number at ₹60,000/month expenses = ₹2.06 crore. At this savings rate, you reach FIRE in approximately 11–12 years, around age 39–40. The key levers are savings rate, starting corpus, and return rate. FIRE on ₹20 LPA is very achievable if you delay major purchases like a primary home (EMI kills savings rate), avoid lifestyle inflation, and invest consistently in equity mutual funds.

Q: How does EPF count toward my FIRE corpus?

EPF (Employees' Provident Fund) absolutely counts toward your FIRE corpus, and is often undervalued. EPF earns 8.25% interest (FY 2024-25) and is extremely tax-efficient — contributions qualify for 80C, earnings are tax-free after 5 years, and withdrawals after retirement are also tax-free. For the purpose of this calculator, add your current EPF balance to the "Total Corpus Today" field. However, note that EPF cannot be withdrawn until age 58 (with some exceptions), so factor in that it is locked for the accumulation phase if you plan to FIRE before 58.

Q: What expected return rate should I use in this calculator?

For a diversified Indian equity portfolio (large-cap + mid-cap mix), historical CAGR over 10+ year periods has been 12–14%. For aggressive small-cap heavy portfolios, 14–16% historically but with higher risk. For conservative portfolios (60% equity + debt), 9–11% is reasonable. Use 10–12% if you are mostly in diversified equity mutual funds. Use 8–9% if you are conservative with significant FD/PPF allocation. Do not use peak recent returns (20%+) for FIRE planning — these are not sustainable long-term.

Q: Should I choose the old or new tax regime for FIRE planning?

For most FIRE-aspiring individuals who invest heavily — especially those maximizing 80C (₹1.5L), 80D (₹25K health insurance), NPS (₹50K under 80CCD(1B)), and HRA exemption — the old regime often saves more tax when annual income is above ₹10–12 LPA. However, for those with simpler finances or income below ₹7.75L (new regime standard deduction + rebate combo), the new regime may be better. The key insight for FIRE: maximising your net-of-tax savings rate matters more than the regime choice. Use ToolForge's Income Tax Estimator to compare both regimes for your specific income and deductions.

Q: How does inflation affect my FIRE corpus calculation?

Inflation is the biggest risk to FIRE planning in India. At 6% annual inflation, today's ₹50,000/month expenses will become ₹1.61 lakh/month in 20 years. The SWR approach inherently accounts for this: your corpus must be large enough to allow annual withdrawals that grow with inflation while the residual continues to compound. This is why using a real (inflation-adjusted) return matters. If your investments earn 12% and inflation is 6%, your real return is approximately 5.7%. The 3.5% SWR is chosen to be sustainable even accounting for a realistic Indian inflation trajectory.

Q: What is Geo-Arbitrage FIRE and is it practical for Indians?

Geo-Arbitrage FIRE (Geo-Arb FIRE) means retiring in a location with a significantly lower cost of living while drawing from an India-based corpus. This works in two ways for Indians: (1) Relocating to a Tier-2/Tier-3 Indian city — expenses in cities like Coimbatore, Jaipur, or Nagpur can be 40–50% lower than Mumbai or Bangalore; (2) Retiring abroad in SE Asian countries like Bali (Indonesia), Thailand, or Vietnam where ₹1–2 lakh/month provides a luxurious lifestyle. The calculator assumes 60% of current expenses for Geo-Arb within India. This dramatically reduces the required corpus and can move your FIRE date 5–10 years earlier.

Q: Is it safe to rely entirely on SIP returns for FIRE planning?

SIPs in equity mutual funds are the most accessible FIRE wealth-building tool for most Indians, but diversification matters for the withdrawal phase. Building up to FIRE predominantly through equity SIPs is sound strategy. However, as you approach and enter retirement, you should gradually shift some corpus to more stable instruments (debt funds, bonds, liquid funds) to reduce sequence-of-returns risk — the risk that a market crash in the first few years of retirement permanently damages your corpus. A common strategy: keep 2–3 years of expenses in liquid/debt funds at all times during retirement, and withdraw from equity only during good market years.

Q: How much corpus do I need to retire at 45 in India?

To retire at 45 in India, you need a corpus of approximately 28–30× your annual retirement expenses, using a 3.5% Safe Withdrawal Rate. For ₹60,000/month (₹7.2 lakh/year) in expenses, the corpus needed is ₹2.06 crore. For ₹1 lakh/month (₹12 lakh/year), you need ₹3.43 crore. Plan for a 40–45 year retirement horizon (age 45 to 85–90), which demands extra conservatism. Key levers to retire at 45 from a typical Indian salary: start investing before 30, maintain a 40–50% savings rate, avoid large EMIs in your 30s, and invest heavily in equity mutual funds. Use the Advanced mode in this calculator and set Life Expectancy to 85 to model this horizon accurately.

Q: How does PPF count toward my FIRE corpus?

PPF (Public Provident Fund) is one of the best FIRE-building instruments for conservative Indian investors. It earns 7.1% interest (current rate), is fully tax-free (EEE — exempt on contribution, growth, and withdrawal), and has sovereign guarantee. For this calculator, add your current PPF balance to the "Total Corpus Today" field. Caveats for FIRE planners: PPF has a 15-year lock-in, extendable in 5-year blocks. Partial withdrawal is allowed after year 7. If you plan to retire before 45, your PPF may still be locked — factor this in as inaccessible for early retirement. However, PPF in your 30s becomes a powerful tax-free retirement fund from age 45 onwards.

Related Tools

Ready to start your FIRE journey?

Start a SIP today to put your FIRE plan into action.

Affiliate link — we may earn a commission at no extra cost to you.

Sources & Methodology

All calculations in this tool are built on publicly available data from Indian regulatory and industry bodies. Key sources:

- →Mutual fund return benchmarks: AMFI India (amfiindia.com) — Association of Mutual Funds in India. Historical NAV and category-average return data.

- →Income tax slabs, rebates & surcharge: Income Tax India portal (incometax.gov.in) — Official CBDT source for Old Regime and New Regime slab rates, Section 87A rebate limits, and surcharge thresholds.

- →Inflation benchmarks (CPI): Reserve Bank of India (rbi.org.in) — CPI inflation data used to derive real return estimates. India's long-run CPI average used as the default 6% inflation assumption.

Safe Withdrawal Rate (SWR) methodology adapts the US-based Trinity Study (Bengen, 1994; Cooley et al., 1998) to Indian market conditions — accounting for higher inflation, rupee depreciation risk, and shorter equity market history. Default SWR of 3.5% reflects the consensus among Indian FIRE researchers.